Access to finance and financial inclusion touch almost all areas of our lives. The ability to pay, save, borrow and send money is an underlying requirement for a multitude of tasks most of us do daily– sending our kids to school, starting or running a business, supporting a family member, paying medical bills and more.

For large segments of people in emerging markets, these are often out of reach or difficult to execute because they lack access to the financial products underpinning all these transactions.

Over the last decade, both governmental and private sector stakeholders in Egypt have put significant efforts into advancing access to finance and financial inclusion, with some critical successes. However, gaps remain.

In this blog post, we want to look at the challenges surrounding access to finance in Egypt and why some of these exclusions persist, how the government has attempted and succeeded in improving financial inclusion and how technology startups are stepping into gaps.

We also want to highlight 2 of or our Fund I portfolio companies; blnk and Moneyfellows, who have managed to crack some of the most critical challenges in financial inclusion in Egypt – namely, how we can better serve the unbanked and how we can design scalable access to financial products outside the conventional loan/credit system.

Financial inclusion and lack of access in Egypt

Up until about 15 years ago, the vast majority of Egyptians was unbanked. The precise numbers are not always easy to come by, as they depend on definitions of “banked” and “financially excluded”. However, the World Bank puts account ownership in Egypt at 10% in 2011, while the CBE puts the financial inclusion rate at 27.4% for 2016. Both entities have recorded a massive rise since then, to ~42% and 76% respectively.

Still critical challenges remain.

Limited access to formal financial services is a particularly acute challenge for people outside of metropolitan areas and those working in the informal sector, which in Egypt are estimated to be over 60% of the working population. In addition to rural populations, women, poor people, and MSMEs also continue to face barriers to access finance.

Egypt ranks among the countries in the world with the highest gender gap when it comes to smartphone ownership, with over 90% of men owning phones and ~65% owning smart phones, compared to only 75% of women owning phones and ~45% owning smartphones, according to the World Bank [1]. The following means that the uneven distribution of the very tools needed to overcome existing access barriers, limits the impact potential of digital tools to reduce inequalities.

Egypt is also the country with the highest share of unbanked people citing a lack of money as the reason they do not have a bank account (90%). Systemic inequalities to access, both due to socioeconomic status and gender, are challenges that remain to be tackled.

Historically, access to financial services in Egypt faced two major gaps. With high rates of unbanked individuals on the one side, but also large numbers of banked but underserved clients, due to a slow and inflexible banking system. The first group largely includes poorer Egyptians who, because of informal work or lack of official documentation, distance from branches, and complex paperwork are often unable to open bank accounts at all. This cuts them off from even basic services such as digital payments or instant money transfers. The second group, people who are banked, often still struggle to access critical financial services, particularly credit due to a lack of minimum balance requirements or missing collateral or formal work contracts, leaving many banked Egyptians underserved.

Key operational challenges to advancing financial inclusion were complex KYC processes, limited interoperability, low customer protection and cybersecurity requirements, eroding trust in digital products and insufficiently stable internet connectivity and smartphone penetration, especially in remote areas.

Government efforts to bring citizens into the formal banking system

Seeing these barriers, the Egyptian government has put significant efforts into driving financial inclusion and advancing digitization in its banking system.

Financial inclusion was made a national priority as part of the Sustainable Development Strategy (SDS): Egypt’s Vision 2030, and in 2022 the Central Bank of Egypt (CBE) issued its first Financial Inclusion Strategy (2022-2025) [2].

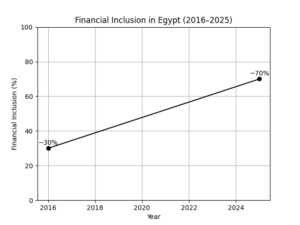

The Central Bank of Egypt’s digital transformation efforts, among other initiatives, have increased individual financial inclusion rates from ~30% in 2016 to ~70% in 2025. Key initiatives included the expansion of online and mobile banking, adoption of national payment systems such as Meeza and mobile wallets, rollout of instant transfer platforms like InstaPay, as well as a reform, streamlining and digitization of CDD/KYC and AML / CTF processes. The mobile interoperability scheme, Ta7weel, introduced in June 2017, has improved interoperability by giving users of different mobile payment schemes the ability to transact with each other directly.

EBC, the national payments network, and domestic scheme operator MEEZA, have enabled full interoperability across payment service providers and all-access channels [3].

Exactly how many people remain unbanked in Egypt is difficult to say, because numbers differ depending on definitions used. But what is clear is that we have seen great progress [4], including among the sub-groups most acutely excluded.

According to the CBE, financial inclusion rates for women, while lower than for men, have risen much sharper – from 19.1% in 2016 to 54.1% in 2022, a growth rate of 192% (versus 131% for men in the same period).

Technology startups stepping into the gap

While these efforts from government and banks have greatly increased the number of Egyptians with bank accounts, private companies, particularly tech startups, have also stepped in to provide additional critical services at scale that the banking system was unable or unwilling to offer. These include point-of-sale financing, microloans for customers with no credit history, mobile wallets, digital platforms that help users build formal credit profiles, or remittance services.

On the back of a sharply increasing smartphone penetration, fintechs across emerging markets have taken on a major challenge: using technology to build products that meet people where they are, serve clients that traditional financial institutions cannot serve, massively scale existing products through digitization, increasing efficiency and lowering cost and access barriers, as well as scaling offline financial habits into online products.

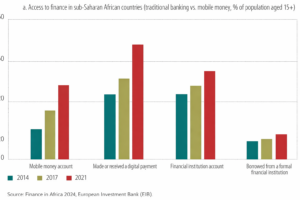

The introduction of mobile money, for example, has almost doubled account ownership across Sub-Saharan Africa between 2011 and 2022 [5]. The share of people with a mobile money account in sub-Saharan Africa has almost tripled from 12% in 2014 to 33% in 2021, driving a large share of the region’s financial inclusion (in the same period the share of people with a traditional financial account grew from 29% to 40%) [6].

In 2022, Africa accounted for more than two-thirds of global mobile financial transactions in volume and value. According to the EIB[7], this number is attributable to the continent’s large young and urban populations, the number of smartphone connections and the presence of digital platforms run by mobile operators, as well as the often-lower cost of digital financial products compared to traditional banking services. This dominance of digital tools over traditional banking leaves massive room for innovation. Several countries on the continent have seen fintech powerhouses rise that have shaped entire ecosystems.

In 2022, Africa accounted for more than two-thirds of global mobile financial transactions in volume and value. According to the EIB[7], this number is attributable to the continent’s large young and urban populations, the number of smartphone connections and the presence of digital platforms run by mobile operators, as well as the often-lower cost of digital financial products compared to traditional banking services. This dominance of digital tools over traditional banking leaves massive room for innovation. Several countries on the continent have seen fintech powerhouses rise that have shaped entire ecosystems.

In Egypt, Fawry expanded access to digital payments by building a nationwide network of merchants and kiosks rather than relying on bank branches, enabling everyday transactions such as bill payments and mobile top-ups in local neighborhoods.

In Kenya, M-PESA, a startup founded in 2006, uses the mobile phone to transfer money domestically and make payments. The company has been highly successful, with more than 84% of Kenyans who are living in poverty using its services, and 40% of Kenya’s GDP going through the company. M-PESA was able to grow very quickly, achieving 1 million customers in just 8 months, and is now serving 16.6 million active customers, or 36% of the country’s population.

Meanwhile in Nigeria, Moniepoint has become one of Africa’s most impactful fintech success stories. The company reached unicorn status in October 2024 after a US $110 million Series C round valuing it at over $1 billion. Today it serves more than 10 million active users and processes over $250 billion in digital payments annually while maintaining its profitability.

Two companies in our Fund I portfolio, blnk and Moneyfellows, are successful local examples of companies bringing innovative financial services to Egyptians who previously lacked access.

So, we sat down with their founders to discuss how their companies and products address key gaps in the Egyptian market, what their biggest lessons learned have been, and what they believe their greatest impact potential is.

blnk: Bringing consumer finance to the unbanked

blnk is an Egyptian consumer finance company that provides installment-based credit at the point of sale through a network of partner merchants. Rather than relying on traditional bank lending, blnk enables customers to finance everyday purchases with simple onboarding and limited documentation.

The company targets individuals typically excluded from formal credit, especially first-time borrowers with no credit history. By using alternative data instead of traditional credit scores, blnk has served over 120,000 clients, 70% of whom were previously unbanked, 36% women, and 38% living outside metropolitan areas.

According to the company’s co-founders, when blnk launched, the market was severely under‑penetrated. While consumer finance companies had seen a massive surge, most of them, like the banks before them, were focusing on customers with a credit history, roughly five million people, a segment in which competition was quite high. Meanwhile, a much larger share of the population, about sixty million adults, were largely ignored. Serving this segment was seen as too risky, because it involves a very large number of small loans and limited data points to assess clients’ repayment capacity. This made it a massively untapped market with tremendous opportunity and impact potential.

To address this gap, blnk fundamentally rethought how credit should be underwritten. According to the co-founders, “it is not just about the data. Two customers can have the same income or live in the same area, but their intentions are completely different. So interpreting the data, and understanding the motivation and behavior behind it, became central to how we underwrite loans.” Based on this insight, the team developed a merchant‑led acquisition model to reach customers directly at the point of sale.

As the company expanded beyond Cairo into Egypt’s provinces, the need for their product became even more apparent. “In remote areas, serving the unbanked had impact built into the product, because we were providing a critical service nobody else was offering. We remained committed to this strategy, targeting unbanked and severely underserved clients first and foremost, because that is where we saw the biggest gap and impact potential. So we never shifted our focus, even during the toughest times in 2022 and 2023, when many people advised us to pivot to more reliable and easy-to-serve segments”.

Targeting customers with no credit history or bank account, which are roughly 70% of blnk’s users, is not an easy undertaking. These are loans that are challenging to underwrite, collect on, and access working capital for. It is also a balancing act between impact and client protection. “The impact potential for our clients is massive, especially for those locked out of the financial system or in remote areas. But our clients are also potentially vulnerable and not financially literate. So it was important for us to build our product in a way that maximizes impact and reaches the largest possible number of clients, while making sure we don’t lend to people who aren’t actually able or willing to repay their loans or who don’t fully understand conditions and consequences”.

The co‑founders also reflected on navigating Egypt’s volatile market “Change is the only constant. From currency devaluation to rising interest rates and changing regulations, we’ve had to adjust everything continuously.” In startups, things rarely go as planned. You have to be willing to shift and react on the fly. Resilience and flexibility determine success. […] You must be willing to do the hard thing that nobody else is doing. Learn by doing, face challenges, and you’ll create impact and growth”.

Money Fellows: A financial system digitizing and scaling savings & lending circles

Many Egyptians are unable or unwilling to access loans from traditional banks, which has created a long-standing need for alternative ways to save and borrow. One such solution is the Gameya, a system that exists in many emerging markets under different names. Traditionally offline, a Gameya works by having participants contribute a fixed amount every month, with one member receiving the full pool on a rotating basis. This allows some participants to save while others effectively borrow, depending on their turn in the cycle. The system has been popular due to its low cost, low risk, and alignment with cultural norms.

However, offline Gameyas are inherently small-scale because it is difficult to find enough trusted participants saving or borrowing similar amounts at the same time. There have been many attempts to digitize this model for scale and to make it more accessible, but the challenge has always been replicating the trust and reliability of the offline system in an online environment.

Money Fellows is the first company in Egypt and world-wide that managed to successfully digitize.

The company addressed offline limitations by creating a mobile app where users can join circles online, have contributions and payouts tracked automatically, and participate with a much wider network across the country.

According to the founder & CEO Ahmed Wadi, the company was able to do what others were not because they “focused meticulously on replicating the trust and reliability of the model online, allowing people of similar financial goals to join circles anywhere, anytime. We have also managed to keep defaults low, by slowly graduating users from later to earlier spots in a cycle. It took us a while and several pivots, but eventually we were able to crack the model, as we continue to improve the experience by personalizing it to cater to our users wants or needs.

According to the founder & CEO Ahmed Wadi, the company was able to do what others were not because they “focused meticulously on replicating the trust and reliability of the model online, allowing people of similar financial goals to join circles anywhere, anytime. We have also managed to keep defaults low, by slowly graduating users from later to earlier spots in a cycle. It took us a while and several pivots, but eventually we were able to crack the model, as we continue to improve the experience by personalizing it to cater to our users wants or needs.

By tracking the lending and borrowing of each user, Money Fellows is in the process to formalize integrating the built-up credit scores of those using the money circles with that of larger financial banking systems, thus improving their chances of obtaining finance from these systems. Essentially, allowing customers off the banking grid to join Money Fellows, build up a credit score through using the app, and then raise their financial profile, making them eligible for more extensive lending opportunities. “We assess them and their financial health … and based on that we allow them to join specific slots and maximum payouts,” Wadi said.

Since its launch, the platform has exceeded 8 million users, with over 2 million rotating savings groups completed through its application.

As of 2025, Money Fellows served around 350,000 monthly active users, serve 26 governorates across Egypt. Additionally, the company has expanded its offering with additional products, including a prepaid card for payouts, repayments, and transactions. As well as collaborating with more than 350 local and regional partners.

To sustain its growth and expansion, Money Fellows is currently preparing to expand to Morocco this year. The company is focusing on markets with strong informal savings cultures and large unbanked populations. In these markets, many people still save and borrow informally, literally keeping money under the mattress. This is especially common among women and those in rural areas, who face even more limited access to formal financial services.

As a result, large portions of the population are excluded from critical financial tools, limiting their ability to plan for the future, save for emergencies, start businesses, or support their families. Digitizing a culturally appropriate savings and lending service that can scale easily in remote areas while maintaining low client risk therefore has enormous built-in impact. According to Wadi, “From what we know about our clients, they often use our service to save for their goals. The biggest goal contribution being ‘Marriage & Housing’ followed by ‘Education’ and ‘Asset & business financing’ then come other goals such as debt consolidation, and travel.

Because even clients who are banked, which make up about 50% of our users, still struggle to access financing from banks for personal expenses like weddings, their children’s education, or other costs without collateral. Yet these are some of the most important expenses for people to live a good life and ensure a better future for their children. Using our product allows them to do that.”

Looking Ahead

What blnk and MoneyFellows show is clear: by grounding innovation in how people manage money, fintechs can expand access to financial tools that previously excluded millions. Egyptians are now saving, borrowing, paying, and planning in ways that were not possible before. This is especially true for those most severely locked out of the financial system, including people in rural areas, those working in the informal economy, and women, all of whom blnk and MoneyFellows can serve in different ways. As these companies continue to scale, introduce new services, and reach more people, they are helping to shape a more inclusive financial landscape in Egypt and beyond.

The number of digital payment users in Egypt is expected to grow to 56.74 million by 2028, about 21% higher than the 46.9 million adults with financial accounts in 2023, showcasing continued progress in digital inclusion. The impact of government efforts to drive formal financial inclusion, as well as tech companies creating and scaling access to finance is massive, because they managed to formalize informal practices, increase trust in digital financial services, and give people access to tools that allow them to plan for their financial future in ways that was previously impossible [8].

What makes some of these products especially compelling is their ability to adapt to real-world behaviors and cultural contexts, proving that financial innovation works best when it meets people where they are. Notably, AI is likely to become a key enabler in the next stage of financial inclusion.

Particularly in markets like Egypt where digital finance adoption already outpaces formal banking access.

While Africa continues to lag behind other regions in traditional bank penetration, it is among the world’s most active users of mobile and digital financial services [9].

Building on this foundation, advances in data analytics and AI allow fintechs to design more tailored and cost-efficient products that reach users with limited or fragmented financial histories. By using alternative data to assess creditworthiness and financial behavior, AI-enabled platforms can extend basic financial services to individuals and small businesses that would otherwise remain excluded. Beyond inclusion, these technologies can also strengthen the broader financial system by improving operational efficiency and supporting more proactive oversight, helping digital finance scale responsibly as participation deepens. Building on these developments, the 2025 Industry Trends Report [10] highlights additional forces impacting Africa’s digital finance landscape. Super apps are increasingly integrating payments, lending, and wealth management into single platforms, simplifying access for users who lack formal bank accounts. Fintech-bank collaborations are also emerging, with traditional banks leveraging AI-driven credit scoring, microloans, and virtual cards to extend services, while fintechs scale through regulatory licenses and partnerships. Investment in predictive analytics, cybersecurity, and digital wallets continues to accelerate, enabling more efficient, secure, and inclusive financial services. These trends suggest that the next phase of financial inclusion Africa will combine AI innovation, platform consolidation, and cross-sector collaboration to reach underserved populations while strengthening the resilience and efficiency of the financial system.

We would like to thank blnk cofounders Amr Sultan, Ahmed Ozalp, and Tarek El Sheikh as well as Moneyfellows founder Ahmed Wadi for sharing their insights and lessons learned for this blog post.

References:

[1] The World Bank (2025): The Global Findex Database 2025: Connectivity and financial inclusion in the digital economy https://www.worldbank.org/en/publication/globalfindex

[2] AFI & CBE (2018): Financial inclusion through digital financial services and fintech: The case of Egypt https://www.afi-global.org/sites/default/files/publications/2018-08/AFI_Egypt_Report_AW_digital.pdf

[4] Central Bank of Egypt: Financial Inclusion Strategy (2022-2025) https://www.cbe.org.eg/-/media/project/cbe/page-content/rich-text/financial-inclusion/main-highlights-of-financial-inclusion-strategy-2022-2025–english.pdf

[5] World Bank (2025): Financial inclusion in Africa: Progress, challenges and the road ahead. https://blogs.worldbank.org/en/developmenttalk/financial-inclusion-in-africa–progress–challenges–and-the-roa0

[6] European Investment Bank (EIB) (2024): Finance in Africa https://www.eib.org/en/publications/20240033-finance-in-africa

[7] European Investment Bank (EIB) (2024): Finance in Africa https://www.eib.org/en/publications/20240033-finance-in-africa

[8] European Investment Bank (EIB) (2024): Finance in Africa https://www.eib.org/en/publications/20240033-finance-in-africa

[9] European Investment Bank (EIB) (2024): Finance in Africa https://www.eib.org/en/publications/20240033-finance-in-africa

[10] 2025 Industry Trends Report https://web.theboardroomafrica.com/wp-content/uploads/2025/03/2025-Industry-Trends-Report.pdf